The United Kingdom has long maintained its status as a premier global hub for international commerce, characterized by a robust legal system, a competitive tax regime, and a transparent regulatory environment. For foreign entrepreneurs, navigating the intricacies of UK company formation requires a multifaceted understanding of corporate law, administrative compliance, and fiscal responsibilities. This article provides an in-depth scholarly examination of the procedures, legal structures, and strategic implications of establishing a business entity in the UK as a non-resident.

1. The Strategic Appeal of the UK Jurisdiction

The United Kingdom’s appeal to international investors is anchored in its adherence to the rule of law and the efficiency of its administrative institutions. According to the World Bank’s historical ‘Ease of Doing Business’ indices, the UK consistently ranks among the top global jurisdictions for starting a business. The primary legislative framework governing corporate entities is the Companies Act 2006, which provides a flexible yet rigorous structure for business operations. For foreign nationals, the absence of citizenship or residency requirements for shareholding and directorship makes the UK an exceptionally accessible market.

2. Selecting the Optimal Corporate Structure

The choice of legal entity is a foundational decision that impacts liability, taxation, and governance. The most prevalent structures for foreign entrepreneurs include:

- Private Limited Company (Ltd): The most common vehicle, where the liability of shareholders is limited to the value of their shares. It offers a distinct legal personality, separate from its owners.

- Limited Liability Partnership (LLP): Frequently utilized by professional services, an LLP combines the flexibility of a partnership with the limited liability protections of a company.

- Public Limited Company (PLC): Suitable for larger enterprises intending to raise capital from the public, requiring a minimum share capital of £50,000.

- Corporation Tax: Companies must register with HMRC and pay tax on taxable profits. The UK offers a competitive rate compared to many OECD peers.

- Value Added Tax (VAT): Registration is mandatory if the annual turnover exceeds a specific threshold (currently £90,000), though voluntary registration is common for businesses seeking to reclaim input tax.

- Double Taxation Treaties: The UK possesses one of the world’s most extensive networks of double taxation treaties. These agreements ensure that foreign entrepreneurs are not taxed twice on the same income in the UK and their home country.

- Confirmation Statement: An annual filing that verifies the accuracy of the information held by Companies House, including details of directors, shareholders, and the ‘Persons with Significant Control’ (PSC) register.

- Statutory Accounts: Even if a company is non-trading (dormant), it must file annual accounts that provide a snapshot of its financial position.

- PSC Register: In an effort to increase corporate transparency and combat money laundering, UK companies must disclose the identities of individuals who exert significant influence or control over the entity.

For most foreign startups, the Private Limited Company is the preferred choice due to its administrative simplicity and the protection it affords personal assets.

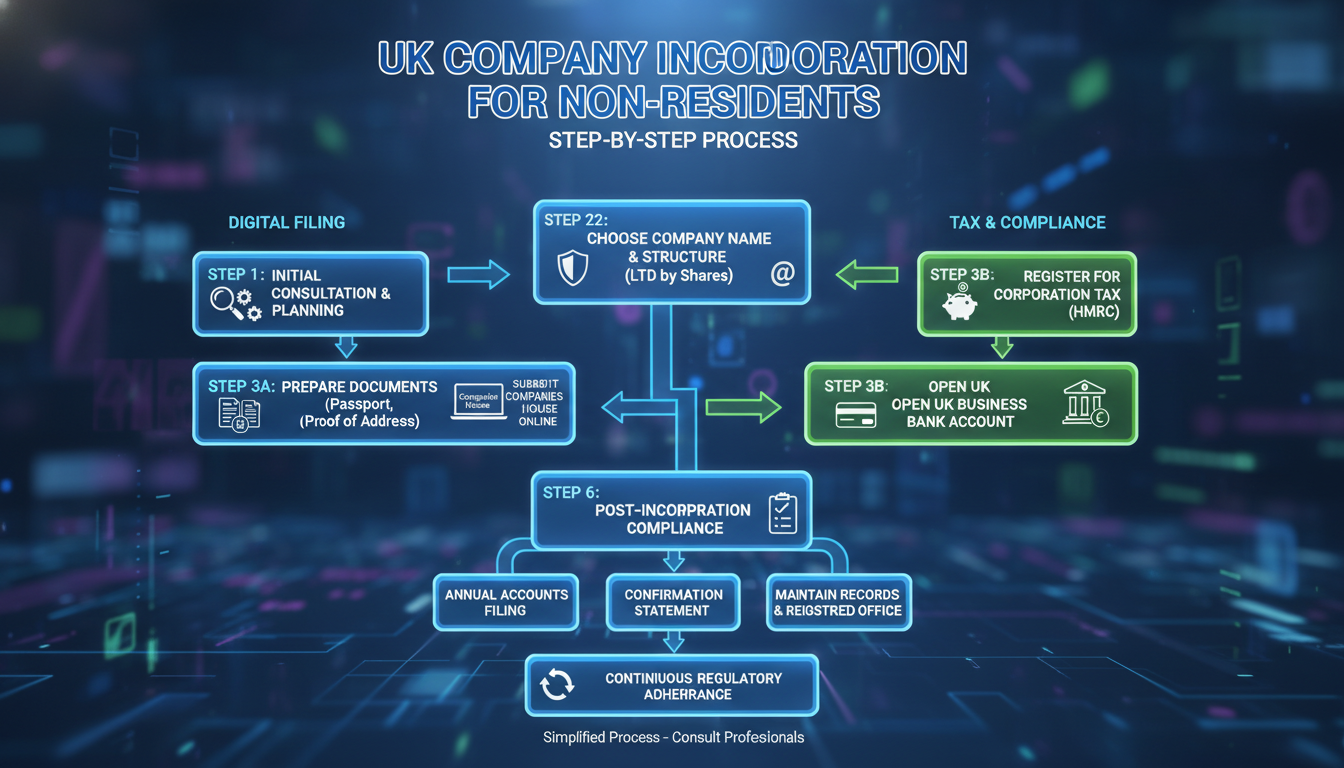

3. The Registration Process: From Documentation to Incorporation

Incorporation is managed by Companies House, the UK’s registrar of companies. The process is remarkably streamlined, often completed within 24 hours via electronic filing. However, the documentation required is specific and must be meticulously prepared.

#

A. Memorandum and Articles of Association

These constitutional documents define the company’s purpose and the internal rules governing the relationship between directors and shareholders. While ‘model articles’ are provided by the government, foreign entrepreneurs often require bespoke articles to address cross-border governance issues.

#

B. Appointment of Officers

A UK company must have at least one director who is a natural person (aged 16 or over). There is no legal requirement for the director to be a UK resident, although having a local director can facilitate certain administrative processes, such as opening a corporate bank account.

#

C. Registered Office Address

Every UK company must maintain a physical registered office address within the UK (England and Wales, Scotland, or Northern Ireland). This address serves as the official point of contact for statutory correspondence from Companies House and HM Revenue & Customs (HMRC). Many foreign entrepreneurs utilize professional ‘virtual office’ services to fulfill this requirement while operating from abroad.

4. Fiscal Obligations and Taxation Framework

Foreign-owned UK companies are subject to the UK’s tax jurisdiction on their worldwide profits. The primary fiscal considerations include:

5. Post-Incorporation Compliance and Governance

Maintaining a company in ‘good standing’ requires ongoing adherence to statutory obligations. Failure to comply can result in financial penalties or the striking off of the company from the register.

6. Challenges in Banking and AML Compliance

Perhaps the most significant hurdle for foreign entrepreneurs is not the incorporation itself, but the acquisition of a UK corporate bank account. UK financial institutions operate under stringent Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations. Banks often require proof of a physical nexus to the UK, such as local contracts, employees, or a resident director. Consequently, many international founders turn to electronic money institutions (EMIs) or neo-banks, which offer more flexible onboarding processes for non-residents.

7. Strategic Synthesis

Establishing a UK company provides foreign entrepreneurs with a prestigious corporate identity and a gateway to European and global markets. However, the process demands more than mere registration; it requires a strategic approach to governance and a commitment to transparency. By leveraging the UK’s stable legal environment and favorable tax treaties, international business owners can build a resilient foundation for global expansion.

In conclusion, while the administrative barriers to entry are low, the complexity of ongoing compliance and the challenges of the banking sector necessitate thorough preparation and, frequently, professional legal and accounting counsel. For the informed entrepreneur, the United Kingdom remains one of the most rewarding jurisdictions for international business ventures.